Being a stay-at-home mom is a full-time job that requires patience, creativity, and hard work. But even with careful budgeting and cutting expenses wherever possible, it can feel impossible to get out of debt.

That’s what happened to me, a stay-at-home mom of two who found herself struggling to keep up with credit card payments and bills.

In fact, I felt like I was struggling in EVERY other area of my life too! It’s funny how those things go hand-in-hand. I feel like everybody who’s desperate to get rid of debt all say the same thing. Which is, when you find yourself struggling with money, you’re struggling in all other areas of your life as well.

But that’s no coincidence. It all boils down to the reason that you ‘re in this position to begin with. Keep reading, because eventually you will get to a point you’ll have no choice but to deal with those reasons. You can only put a Band-Aid on your personal finances for so long.

But that’s ok! IT WILL BE OK. Nothing to fear but fear itself…. right?

You got this and I got you! So, let’s get comfortable – go grab a coffee or a glass of wine, I’ll wait! Hey, it’s 5 o’clock somewhere!

Whatever you do, don’t skim through this guide like a bat out of hell! When you read this guide slowly, you WILL give your brain more time to process the information, which leads to better comprehension of the process.

This will help you avoid making mistakes and just ensures that you fully understand what you’re supposed to do. Don’t rush yourself.

I don’t want you to miss out on any important details or skip over important steps. Each one – big or small – counts. These are the steps which are going to help you create a budget efficiently and effectively, so that you learn how to get out of debt fast.

You don’t need to spend even more money on debt relief programs or other debt settlement options. Absolutely not. The answer to saving money is not spending more money! This makes me laugh!

There are ways to reduce debt without rushing out and getting a debt consolidation loan! Please don’t do this. Sometimes, it can be helpful as a last resort option. I get it. Sometimes you just gotta do what you gotta do.

But before you even think about going down that path, I want you to go through all my debt-free living tips and other debt management strategies. Perhaps you’ve been considering student loan debt forgiveness or credit card debt consolidation? Well, its absolutely nothing to be ashamed of.

Debt is debt, no matter where it stems from and how we manage it. We just have to figure out the easiest ways to budget our money and the rest will fall into place.

From Bad to Worse

OMG I was the worst of the worst when it came to, not only spending money, but saving money in general. But I worked my ass off to learn DIY debt consolidation and budgeting for debt repayment.

I would be online all the time looking for bankruptcy alternatives. My credit began to take a huge hit and everything was just falling apart at once.

One day I’m looking at financial planning for debt repayment, and the next day there I am desperately needing bad credit debt consolidation! Yup, in the world of debt management, things can go from zero-to-sixty in a blink of an eye!

It’s so, so important to get a grasp on the situation before it gets any worse. Trust me, that’s not just something people say. I completely understand the severity of that statement now.

It was embarrassing; my credit got so bad that I couldn’t even get a debt consolidation loan. The credit counselling services didn’t even want to deal with me! They expected me to improve my credit so that I could utilize their service, meant to improve my credit….??? *Insert face slap here*

It just continued to go from bad to worse. I felt like I was literally running around in circles. Talk about frustration!

Eventually, after what felt like months and months of research, I started noticing patterns and things kind of started to click for me. I did a lot of trial and error, while reading a lot of debt payoff success stories. It was very inspiring, which did help me.

What used to feel confusing, difficult and impossible – turned into an invigorating feeling of freedom. I am on a debt-free journey now, I don’t have to wake up and go to bed constantly worrying about what bill might come in the mail today.

Financial planning became, well, kind of FUN. Now, now, I hear your gags! Lol.

Did I ever think that I’d be using those words in the SAME sentence, financial planning and fun? Goodness, not a chance! Nope, I would’ve bet money against it.

Determined to get my family’s finances back on track, I decided to take matters into my own hands and eventually I was able to produce an easy-to-follow, bulletproof plan to get out of debt. I realized that creating a personal budget was going to be my saving grace.

The problem was, I didn’t know where or how to start.

“Me, a Budgeter?” I said to myself. Hell no! I wouldn’t be in this situation in the first place if I knew how to budget. I thought no way am I going to be able to start now.

But, little by little, I DID start to track my expenses, creating a budget, and even finding ways to increase my income from home. With persistence and a little bit of sacrifice, I was able to pay off my debt and achieve financial freedom for my family.

My 8 Steps to Get out of Debt

Today I am going to be sharing with you that very same 8 step formula that other people are using too, to save $500 or more every single month. Steps you need to know to create and stick to a real budget.

I know that my results were impressive. So that’s why I really want to help you achieve the same results. It feels amazing. If I had to describe it, in just one word: light.

But, I suppose that’s what they mean when they say “a weight has been lifted off my shoulders”. It’s really true, it does feel like that.

O.k., enough rambling Maya, and let’s get down to business!

I’m going to walk you through the following 8 steps so that you can get started with the same budget that got me $102,000 out of debt, in record time!

Before we start, here are some crazy numbers for you.

20 years ago, 65% of people were living paycheck to paycheck.

Fast forward to today, and we are getting worse not better!

Almost 80% of people out there are living paycheck to paycheck.

But here is something that is even crazier.

They did a study showing that for each person making $150,000 a year, 1 in 4 are living paycheck to paycheck. So, think about that. You’re making really good money, but yet you are living paycheck to paycheck. Is it just me or is there something VERY wrong with that picture! Maddening, isn’t it?

The “B” Word

Let’s face it; we all know how quickly money can slip away. We think if we make more, our financial problems will be solved but that is not the case, and you can thank Parkinson’s Law for that – which tells us that as soon as our income rises, so does our spending. But what many do not realize is that there IS a solution – *drumroll* – and it is called budgeting!

Sure, hearing that scary “b-word” may cause you some stress — trust me I have been there too — but just remember, mastering finances does not have to mean sacrifice and it does not mean deprivation either. You will thank yourself in the end for having courage and taking control of where YOUR hard-earned money goes.

I am sure you are thinking, who is this person and what makes her think she can help me. Understood! I am just someone who is obsessed with making money and saving money.

Have been trying to figure out for years what to do with this passion of mine, and well, you are looking at it! I have been there, I have done that, and I know that with my knowledge and experience I can help others like you take control of their money and their life. Otherwise, your money controls you; a 5-star recipe for unhappiness and despair.

My Monthly Budget Plan

We all know how it goes – you want a raise, but your boss just won’t budge. Well scrap that because I am giving you something much better: THE biggest raise of all!

So let us get acquainted with that dreaded B-word together and simplify the whole dang thing! There does not need to be any confusion – budgets do not have to involve crazy spreadsheets or precious time wasted trying to understand how to make them work for you.

I can help you create an effective budget faster than ever before by following my simple system, plus I’ve got cash flow forms ready for you below.

Do not worry, I am not trying to sell you anything either! I get excited about this stuff, like those overly eager hosts on those 2 a.m. infomercials – minus the “if you act right now” sales pitch of course! Haha.

So, let me show you how taking control can result in the greatest financial reward yet; c’mon now, what are ya waiting for?

…..it’s goooooo time!

Step 1 – Financial Statements

As I have said, there are 8 steps to getting a grip on your finances. To start, you will need to take the plunge and look at where you have been spending your money over the last 90 days.

Go ahead, open those bank statements and anything else you might have to show where your money is going. Look at your bank account, your debits, your credits, the fees you are paying…. everything!

It can be intimidating to say the least, but taking an honest look at what is going on is the best way to understand where those funds have gone and why.

Uncle Ben famously told Peter, “With great power comes great responsibility.” This means that if you can do something, do it right and do it for good. Don’t take it for granted.

With that being said, if you know how to budget, do it; do it right and do it well! Don’t take your newfound skills for granted! It’s knowledge that many people wish to have.

Alright, so now that you know how much wiggle room you have, there’s no time to waste – it’s time my friend.

Time to create a budget!

Let’s face it, for most of us budgeting is simply logging into our checking account 5 or 6 times a day to see the balance to make sure we have enough money or just to make sure it is still there! Because if one day for whatever reason, it was gone, how would you feel?

Listen, you do not have to live in fear of your finances disappearing! I can help you get organized and make smarter money decisions.

First, let us go back to the 90 days and examine where your income is coming from, as well as what it is being spent on.

Print out statements for each account, for each month, for the last 3 months.

Step 2 – Create Categories

Now, you’re going to think about and make a list of categories to help organize all your expenses. Do not worry, I have listed pre-set categories if you prefer, which will be provided for you in the budget forms I am giving you.

Being organized is essential for success, but it can prove difficult to achieve. So, to begin this strategy and help you start budgeting your finances, you will categorize all your expenses.

Because understanding where your money comes from and where it goes is essential for taking control of it.

An example of a category might be “transportation”. Then, under this category, you would include expenses such as fuel, oil change, car repairs, car payments, bus passes, etc.

Step 3 – Assign Your Expenses

Now, I want you to go and list each expense under the category it belongs to. If you are unsure, take your best guess – or ask your spouse or a friend!

Go through and compare each month. Look for potential spending habits. Which expenses are consistent, month-to-month?

Step 4 – Circle Same Expenses

Circle expenses that come up every month. For example, you might see that every month you have a cell phone bill. Circle the cell phone bill. You might pay for gas every month. Circle all your gas payments. A quick stop at the grocery store? Circle every grocery purchase! You get the picture 🙂

So, what patterns did you see? Your mortgage, rent, credit card payments, insurance, cell phone bill, a cable bill; any expense that shows up each month.

O.k., so far, we have conquered:

Gathering the last 3 months of bank statements. We created categories to list each expense under and compared each of the 3 months, side by side. We looked at the categories and circled the same expenses each month; consistent spending, something we bought every month, for each of those 3 months.

Now we are going to enter everything that we just circled on our budget, on the forms I have provided. These are excellent, free tools that you can use so that you do this seamlessly.

Step 5 – Combine the Expenses

You will also want to know how much you have been spending in each category.

So, everything that we circled, under each category, we are going to add up. Again, only add up the circled expenses from each category, to find out how much you are spending in each.

Step 6 – Divide and Conquer

You will then divide the total amount by 3, which will then give you your monthly average spending, under each category.

Why a monthly average? Well, it is better to look at the average of the last three months than it is to just look back at the last 30 days. Perhaps you were on vacation or life was a bit different then, you just never know.

We want to get a broader scope, so that is why I want you to go back 90 days and not just 30 days.

So, if for example, you look back and see that you spent a total of $1,500 on groceries over the last 90 days, you are going to take that amount (or whatever it may be for you) and you’re going to divide it by 3; so, $1,500 divided by 3 would be $500.

In this case, we would say that our average monthly grocery bill is $500 per month.

Voila!

Continue to define the categories that match your lifestyle and then track expenses for 90 days to find out what you typically spend in each area. From groceries to going out…it is up to you how detailed or broad these segments are – there is no right or wrong way.

Step 7 – Take-home Pay

Finally, calculate your take-home pay; this is not always equal to your salary when taxes and other things come into play! Whatever you have left after all deductions will accurately show the available funds you have for spending.

Inside the budget forms I am going to give you, there is a category called income. So, where it shows ‘Income’, I want you to write in that number; your take-home pay.

So now you have a good-lookin’ organized budget. You have your income at the top, and then going down you will have all the distinct categories.

Step 8 – Flatline Your Budget

The next step number we are going to “flatline your budget”. What does that mean? Well, what we are creating here is a zero-dollar based budget. Do not worry, it’s just a financial term, which means that the money you have coming IN equals the amount of money that you have going OUT.

You see, we’re telling every dollar what to do before the month starts. In other words, you are going to be PROACTIVE. Whereas most people are RE-ACTIVE. If you are living paycheck to paycheck, you are more likely to fall into the “re-active” group.

80% of the world is reactive, meaning we get to the end of the month, and we think, “holy sh!t, where did all of our money go?” Sound familiar?

Well, instead of doing that now, you will know just how much money you have coming in and you are going to tell every single dollar what to do (even before you have it!).

Some of it might be for rent, a car payment (or 2!), or going out to eat. Whatever it is, we are going to tell every dollar what to do before we spend it. However, here is the problem with that. Do you think the first time you sit down and do this, that magically everything you have set up based on those last 90 days is going to equal your income, every time?

I don’t think so Tim! In fact, 9 times out of 10, you are going to overspent before you even start the budget. This is the budgeting part that everybody freaks out about. I promise you though, it’s not that hard. And again, if you don’t create a budget, eventually you will run out of money, and you’ll be forced to create some kind of budget anyways!

So, you are going to be proactive, okay? what you are going to do is look back and say, based on those last 90 days, maybe it’s $500 off (meaning you’re actually spending $500 more than what you have coming in

So, what we do now is we go through the budget and say, okay, what are some of the things that maybe we could cut back on? Areas where you may be overspending, a little bit or a lot.

What you’ll find out here, a lot of times, is when you go back on the 3 months, you are GOING TO find expenses that you forgot about.

You see, when you do not pay attention to the finances, they build up slowly enough that you don’t even notice. For example, my sister did this recently only to find FREE MONEY! How? From a subscription she had signed up for, two years ago, and did not even know she was paying it! After cancelling that, she suddenly had more money every month.

Another notable example is that I worked with somebody recently, who had not one, not two, but they had THREE Netflix accounts under three different email addresses. She had been doing this for almost 4 years!

Think about all that wasted money. If she were paying attention to her personal finances in the first place, she would have caught it immediately!

But in this case, all she could do was be grateful that she caught it when she did and move forward with a smile on her face knowing that she was going to have all this extra money each month now.

So you are going to go through your own expenses, and you’re going to start seeing things that you really didn’t see or consider before. Maybe you don’t need that premium cable package (you only watch the same 2 channels anyways), or you are eating out too much and did not realize how much it was costing.

Whatever it may be, this is your decision, because it’s your budget.

Regardless, you are going to separate the needs versus the wants. All we are trying to do here is say, okay, if $6,000 is coming in each month, then we must make sure we plan to send $6,000 out.

Because if you plan to send $6,500 out, that means you overspent by $500. In that case, you are simply digging yourself a hole further and further, every single month.

So, let’s recap our steps together.

Step 1 – Gather all financial statements, for the last 3 months.

Step 2 – Create categories.

Step 3 – Assign every expense to a category. Do this for each month.

Step 4 – Circle any expenses that come up every month.

Step 5 – Add up all the circles’ expenses, for each category.

Step 6 – Divide each amount by 3.

Step 7 – Calculate your take-home pay.

Step 8 – Flatline your budget (what goes in must come out!)

You are going to follow your plan on how you want to spend your money.

I had a friend one time that said, Maya, I want to spend $500 a month at Tim Hortons. Well, that’s her call. No judgement, it’s her money!

No one should ever tell you how to spend your money. You are the one that goes to work, and the one who makes sacrifices to do so.

You should do what you want with it, okay? Of course, there’s various exceptions when you’re married, with kids, etc.

Regardless of this, once you and your partner have taken care of the household expenses and what not, you still must have your own money. I simply can not stress how important this is (whether you are a man or woman).

Take control of how you make and use your money! Your wealth is in your hands, so set a plan for success.

Do not let anyone else dictate what to do with the fruits of all that challenging work – they will not be putting it in the bank for you.

Budgeting for Beginners

Finally, you’re probably going to have to adjust here and there. Because within that first month, you will notice things like you already overspent on groceries or did not allocate enough here or maybe you have too much over there. Newsflash, that is normal! The problem is, when we get to this point, we think we failed, so we give up and we don’t bother doing it at all.

Don’t beat yourself up! This is going to happen to you. In fact, 100% of the time, this is going to happen to you! So, you will need to adjust for the first while and that’s ok.

Remember, this first month is a trial month. It’s 30 days where you are just testing the waters. So do not get hard on yourself.

Do not be alarmed if within those first couple of months, you may have to make several adjustments, ok? It’s nothing to worry about. You didn’t do anything “wrong”.

Think about this – even if you did (which you didn’t, but if you did) what’s the worst thing that can happen? You’re attempting to make a budget dear; you’re not trying to prevent WW3.

So do not fret my pet, because it’s a natural process with learning curves like anything else. You can’t even look at it like it was time wasted, because it wasn’t. That’s like saying school was time wasted. Time spent learning is not wasted time.

A month or two from now, you’re going to realize things like hmmm, I did not have enough money saved here, and I put too much over there, etc. But by month three, it all comes together. If you make it to month three, which you will, you will be fine, my dear.

You see, every single month, this gets easier and easier. I can tell you that in the very beginning, when *I* created my budget, it had to have taken me 2-3 hours to set up! My head was spinning.

If you are reading this, it means you are already well ahead of where I was at the beginning. I do not want to come off sounding too cliche, but get ready for it, because this is one of those “If I can do it, you can do it” moments!

But now, oh my gosh, it takes me 10 minutes tops – a month! Yes! Five short but sweet minutes every single month. 5 minutes each month to stay out of debt for the rest of my life, build wealth, and live without any financial stress.

In fact, I tell people that when my head hits the pillow at night, I fall asleep immediately. How? I do not worry about money anymore. I know what is going on with every dollar that I have. It is that simple.

This is like that part of brain is a little locked box now, and when I open it up its meticulously organized, filed and stamped. This used to be an unlocked box, containing a disorganized mess of dysfunction!

Trust me, it is an amazing feeling that you can achieve with extraordinarily little effort! However, most people are simply too scared to investigate their personal finances that closely….and trust me, I GET IT! Boy, do I get it.

Although I am telling you right now, you will only wish that you had done so sooner. Because it feels like 1000 lbs. was lifted off your shoulders! I do not know a better way to explain it.

You see, when you create a budget, you are being proactive. The number one habit of the most successful people on earth is they are proactive.

Instead of wondering what happened to your money at the end of the month, now you are going to tell your money what to do.

Rather than your money controlling you, you will now control your money. You will no longer let life control you…. you will be in control of your life.

Most people will never acknowledge the budget word because of fear; fear of what they will see, fear of what they will not see, and fear of what they will learn about themselves. Fear truly does hold us back, in every aspect of life. But not you, not this, and certainly not today!

O.k., so get those budgeting forms that I made for you, which I personally use as well. Print off as many as you need. I’m giving them to you completely free.

Debt, Debt Baby…..

As you begin to pay off debt, you are going to be amazed at how much money you have left at the end of the month. Paying off multiple debts, so that you can begin to live debt free, can feel overwhelming (don’t I know it!) but the good thing is, it is much easier than it seems – especially when you implement proven strategies.

As you begin to make progress, it will feel as though you are earning more money. You are not actually making money though; you are just saving money – but they are two of the same. More “disposable income” is still income!

By applying the following tips to pay off debt quicker, chances are you will be debt-free much sooner than you could have ever anticipated. Either way, you have nothing to lose and a whole lot more to gain!

I am going to go over some of my best ways to save money.

So, if you are one of those people (and God knows there are many!) who lay awake all-night thinking about how to get rid of debt quickly (and permanently) then you are gonna wanna perk ‘yer ears for this one!

So…. let’s not waste another minute being poor!

Get out of Credit Card Debt

Yes, I know, you’ve all heard this one before!

But the single most important part of being able to pay off debt is:

*drumroll please*

Not being tempted to make any more debt!

Seems simple enough, but as Forest Gump said, “stupid is as stupid does.”

So, if overspending is causing you to make unnecessary purchases and borrow more money, it might be in your best interest to cut up all your credit cards, or at the very least, remove them from your wallet all together!

The average credit card holder has almost $6,000 of credit card debt, according to Moneygeek.com, and with interest rates often reaching or exceeding 30%, this is a problem that should be addressed. Whether we want to face it or not!

Buying items on credit cards feels like free money sometimes, doesn’t it? Sure, you do not need to pay in full immediately, but once those balances start accruing interest, they become almost impossible to pay off! You can barely make the minimum payments because the payments you are making are entirely made up of the interest itself!

Realizing you can be content without spending money way beyond your means is a trait that will help you in many ways. But being happy with what you have does not mean you are never allowed to want for something more.

A nicer car, a bigger home, or a newer phone? Honestly think about the cost of the item and determine just how much value it is going to provide you.

For example, you might want a larger home because it would be nice to have the extra space, sure, but it is going to come with a steep price tag that will double your monthly housing cost.

The new house would certainly be an improvement on your current house, but is it worth the money required?

The same thought process should be applied to other purchases like a new vehicle. Everyone loves a brand-new car! The look, the smell, the style…. who doesn’t love a new car?

But remember, with a new car comes a new payment and all the costs involved that come with it. You might just decide that it is not a great decision.

Looking at the whole picture and weighing all the pros and cons might help you make an educated decision. One that you will be less inclined to race out and spend the money. You might even decide to sell some of what you have.

Debt Repayment Strategy

Implementing a strategy that will guide you through the debt payoff process is a critical step. There is a popular method called the debt snowball. This entails paying off your smallest debt first, such as a store credit card. You will throw all your extra money towards your smallest loan, while still making minimum payments on all other debts.

Once the smallest loan is paid in full, you will focus on the second smallest debt and then the third smallest debt, and so on and so forth. The last debt you will pay off will be the largest debt, like a car or your mortgage.

Another option is to utilize the debt avalanche which suggests you pay down debts in the order of the highest interest rate to the lowest interest rate.

Regardless of the balance, you will focus on paying down the high interest debts first and paying off the low interest rate loans last.

Whether you use one of these strategies or develop your own plan, having some sort of direction will help you stay on track instead of trying to pay off every debt at once.

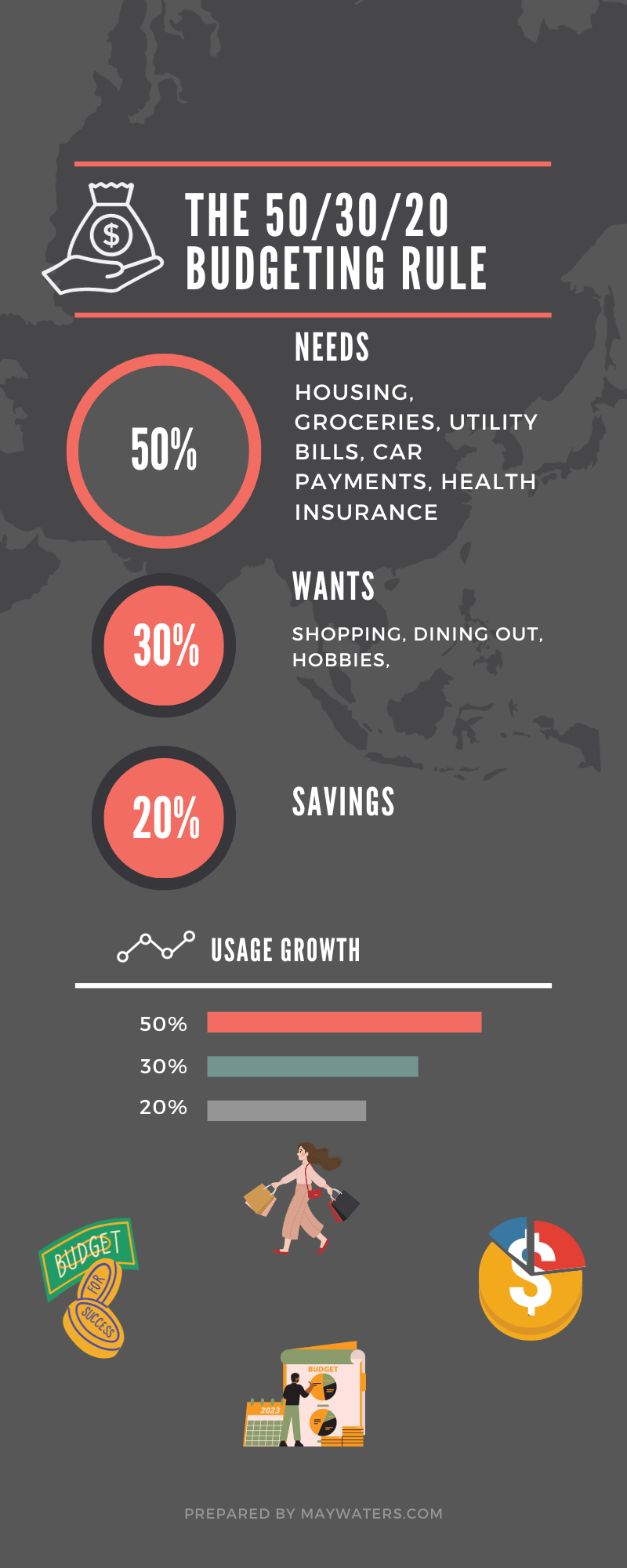

The 50-30-20 Method

Creating a budget, or at least understanding your income and expenses, is always a clever idea, but it is even more important when you are trying to dig yourself out of a hole.

Having a solid understanding of your income and expenses is not just for poor people. Rich people do this as well. You should know where your money is being spent so that you can determine how to make adjustments that will help you carry out your plan.

Many people are surprised at how much money they are throwing away once they keep track of exactly where it is going.

Keep essential expenses, such as housing and necessities, at 50% of your income or below. Allocate 30% for wants and 20% for savings, investments, and debt paydown.

You can adjust, but this is a good place to begin if you are wondering why you are completely broke at the end of the month. Most people who begin using a budget in one form or another feel that they have found money that otherwise would have been lost.

Money Management Tips

Simply put, a lack of money is caused by two things, spending too much money, and not earning enough.

Carefully analyzing spending is critical because even someone who makes $1 million per year could be broke if their spending is out of control.

Increasing your income is also especially important, but of course this is easier said than done. There are a few easy approaches you could take to bring in more money.

These include requesting a raise at work if you feel you are being underpaid considering market rates for your position. Perhaps you have not had a raise in many years despite extensive experience or new hires are being paid much more for the same exact job.

I have a friend who is in this very position right now! His employer’s competition is offering to pay him more money and he is going to be changing companies.

Putting in a few more hours every week, whether you are an employee or have your own business, could make an enormous difference in your ability to pay down debt.

Furthermore, think about creating an additional income stream outside of your main job. This does not necessarily mean taking on another full-time job. It could simply be a couple of hours per week at another job or working for yourself.

Paying more than the minimum payment every month will help you progress towards becoming debt-free. When you make a minimum payment, it has been made up of interest and principal, but when making larger payments, all the extra money goes directly towards reducing the balance.

For example, if you make a regular minimum payment but add $300 to it, the $300 you added on top of the minimum payment would go directly towards reducing your debt.

In fact, credit card companies secretly hate it when customers do this! So, if that is the case, then you know it is a good thing!

I mean, just think about how long you are going to be in debt by not making larger than required payments. By only making the minimum payment required, you are going to draw the length of each loan out to its full term, which raises the cost of the loan considerably.

Making payments more often can be an extremely helpful tip when trying to pay off your debt. Let’s say you have an extra $50 that you are planning to apply towards your debt when you make your next payment.

Well, you could leave the money in your checking account until next month when the bill comes due, provided it is still there. Or, if you have an extra $50 in your account, instead of saying to yourself, I will put that extra $50 towards the bill when it is due, just apply it towards the loan balance right away instead! Before you end up spending it on something else!

A common behavior is that people end up spending money that is left sitting idle, as it tends to burn a hole in their pocket.

Seeing that money in your account will make you feel wealthier, and you will subconsciously see that as extra spending money. Yes, the mind is a beautiful, sneaky thing, isn’t it? Lol.

Putting extra money that you have, over and above what the minimum payments are, could also save you a lot of interest.

Paying off debt can take a long time depending on how many debts you have and how large they are. One of the keys to having a successful debt payoff journey is to stay motivated.

Losing motivation halfway through could cause you to end up back at square one with a mountain of debt.

Think of how your finances will look once you become debt-free and how much money you are going to have to enjoy and invest. Focus on why you want to be debt-free and how it will make your life so much easier and more enjoyable.

Keep track of your progress as you make payments over time. You can feel like you have not made much progress, but if you look at the big picture and see how it looks over time, it will be much more apparent.

Setting goals of when you would like to have a particular debt paid off, when you would like to become debt free, and what will be different once accomplishing this goal will help you keep that end goal in mind. This way, it will be much easier to stay course.

You are going to see more progress towards becoming debt free when you use these proven tips. They will require a little effort on your part, but the result of living a life free of debt is going to have many benefits.

Instead of wasting endless dollars on interest in the bank, you can begin to invest and earn interest of your own, which will give you more free time, allow you to travel, and buy things that are important to you.

I have SO many more goodies in store for you, while at the same time helping you bid goodbye to ALL your money worries.

I’m curious. Is there anything that you have had to give up completely, simply because it was not in your budget? Tell me in the comments below – I love interacting with you guys!

In fact, I would love for you to join our little community by subscribing to my free newsletter. You’ll get an email directly from me (and only me) once a week.